A surety bond is a contract between a debtor and a creditor. A person commits to the creditor to guarantee the payment of a debt contracted by the debtor. The debt must be a debt of money.

Guarantors can be legal entities or individuals. Guarantees forwards, minors, and persons under the moratorium are strictly forbidden.

The guarantee shares the fate of the debt and follows it as an accessory right

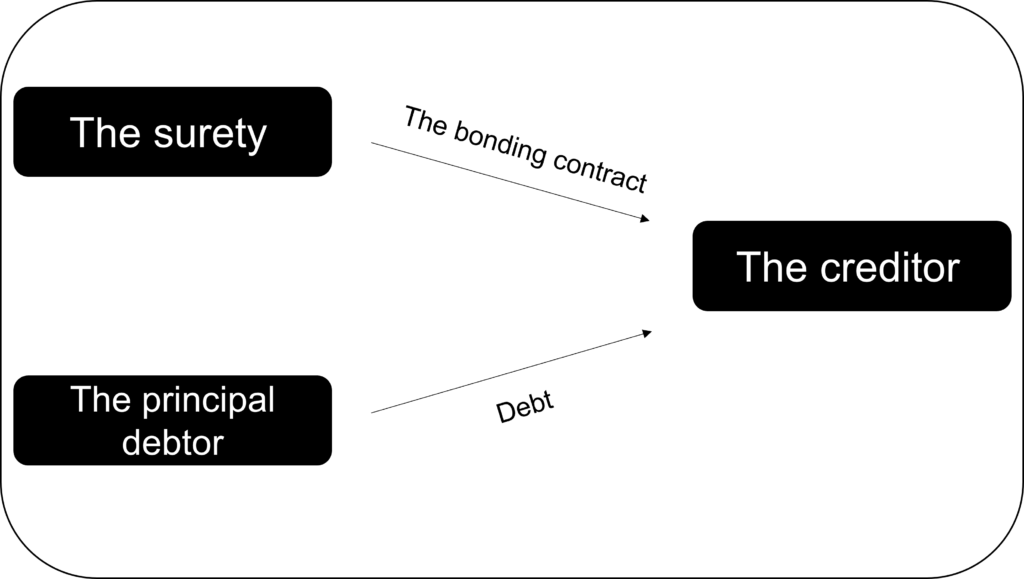

The surety is a construction between three persons: the surety, the creditor, and the principal debtor with the creditor occupying a central place in this exchange (see Figure 1). According to article 492 paragraph 2 of the Swiss Code of Obligations, the accessory nature of a surety bond is defined as follows: "A surety bond can only exist on a valid obligation. A future or conditional obligation may be guaranteed if it becomes effective.

Figure 1 : Scheme on the construction of the guarantee - Swiss Banking Law Manual

The accessory nature of the guarantee is expressed by the fact that the guarantor can raise all the exceptions and objections that result from the debt relationship. The cancellation of this debt must be notified to the debtor as well as to the surety.

The rights of the surety

The surety may not renounce in advance the rights granted to him, but a later renunciation may be allowed. For example, if a surety bond is granted to secure an existing debt, it will be an acknowledgment of debt and the current prescription will be interrupted

Several requirements must be respected

To be valid, the guarantee must meet the following requirements:

The written form

The maximum amount

The name of the creditor

The signature of the surety

Indication of the guaranteed debt

The declaration of willingness to commit as a guarantor

Declarations of guaranty by individuals whose commitment exceeds CHF 2'000 require an authenticated form. The same applies to an increase in the amount of the commitment or the transformation of a simple guarantee into a joint and several guarantees. For other modifications such as the creation of a guarantee by a legal person or a commercial company, the written form will be sufficient.

For married persons, the modification of the guarantee can only be done if the spouse gives his consent. However, those who are not subject to this requirement are legally separated spouses, persons registered in the commercial register, owners of a private company, or as well as managers of a limited liability company.

Types of bonds

Simple Surety Bond

This is characterized by the fact that the guarantor can only be called upon after the creditor has found the debtor. The creditor can only demand payment if the debtor is bankrupt, has obtained a debt-restructuring moratorium, has a definitive certificate of default, and has transferred his residence abroad.

Joint and several guarantees

The joint and several guarantors can be sued before the search for the debtor and the realization of his real estate pledges, but on the condition that the debtor is in default with the payment of his debt. In other words, as soon as the debtor is in default, at the time of the first unpaid amount, the joint and several guarantors undertake to guarantee the defaults of the debt.

Joint guarantee

In the case of a simple joint guarantee, each guarantor is obliged for his share and as a guarantor for the share of the others. On the other hand, in the case of a joint and several guarantees, the guarantors commit themselves to the totality of the creditor's debt.

Surety certifier and back surety

In this case, the debt by the guarantor is guaranteed. The creditor will be covered in the event of the guarantor's insolvency. The guarantor has a right of recourse against the guarantor but also against the debtor.

As for the backup surety, it offers a guarantee to the surety and not to the creditor. Once the guarantor has taken action, he has a right to recovery after the payment against the principal debtor.

The "cautionnement romand" as an alternative in French-speaking Switzerland?

The "cautionnement romand" is an institution that carries out the missions conferred on it by the federal law of October 6, 2006, on financial assistance to guarantee organizations for small and medium-sized enterprises.

It can therefore guarantee operating or investment loans for individuals or companies to enable them to maintain an activity and develop jobs in the cantons of Fribourg, Vaud, Valais, Neuchâtel, and Geneva.

What are the conditions to be met to benefit from the "cautionnement romand"?

The maximum amount of the guaranteed credit is CHF 1'000'000.

Amortization period: 1 to 10 years.

Registration fee: CHF 300, which will be deducted in case of acceptance

One-time contribution to the expertise costs: 1% of the guaranteed credit (minimum CHF 500 and maximum CHF 2'700)

Risk premium: 1.25%.

Fixed fee for management and follow-up of the file: CHF 250

The applicant must first contact his bank to obtain a guaranteed loan. Applications must be made to the cantonal branch of the company's headquarters. You must fill out a bond application form and attach all the documents and information required for the expertise as well as the registration fee. Once these elements have been received, expertise will be opened.

What is the reason for choosing a surety bond?

If we take the example of a rental, the surety bond is intended for all types of renters, whether they are individuals or professionals. All are concerned about the rental guarantee. Companies rent their offices, whether they are warehouses or offices.

The first solution is a bank deposit. The problem lies in the fact that the amount of the rent guarantee will often amount to 6 months for a commercial lease. This solution will generate a huge loss of income.

The deposit allows companies to put the money back into the production machine. This money represents a real source of investment. The money saved can be transformed into a cash flow that can pay off debts or maintain a cash reserve. For example, this money can be used to invest in communication, payment of suppliers, or purchase of goods.

By choosing this new form of guarantee, you opt for financial freedom and cash flow optimization.

The PrestaFlex team will guide you to the right solutions according to your needs. That's why we have the resources to guarantee you a professional and quality service.

If you wish to obtain a loan to develop, innovate or invest in your company, we invite you to contact our teams on the website via the contact section. We handle your projects in the German and French-speaking parts of Switzerland and we offer you tailor-made financing and leasing solutions adapted to your situation.

"

["post_title"]=>

string(70) "Why does the bond change the guarantees for individuals and companies?"

["post_excerpt"]=>

string(308) "Why does the surety bond change the guarantees for individuals and companies?

A surety bond is a contract between a debtor and a creditor. A person commits to the creditor to guarantee the payment of a debt contracted by the debtor. The debt must be a debt of money.

Discover its advantages in the article."

["post_status"]=>

string(7) "publish"

["comment_status"]=>

string(6) "closed"

["ping_status"]=>

string(6) "closed"

["post_password"]=>

string(0) ""

["post_name"]=>

string(69) "why-does-the-bond-change-the-guarantees-for-individuals-and-companies"

["to_ping"]=>

string(0) ""

["pinged"]=>

string(0) ""

["post_modified"]=>

string(19) "2022-09-20 11:18:29"

["post_modified_gmt"]=>

string(19) "2022-09-20 09:18:29"

["post_content_filtered"]=>

string(0) ""

["post_parent"]=>

int(0)

["guid"]=>

string(29) "https://prestaflex.ch/?p=5683"

["menu_order"]=>

int(0)

["post_type"]=>

string(4) "post"

["post_mime_type"]=>

string(0) ""

["comment_count"]=>

string(1) "0"

["filter"]=>

string(3) "raw"

}

A surety bond is a contract between a debtor and a creditor. A person commits to the creditor to guarantee the payment of a debt contracted by the debtor. The debt must be a debt of money.

Guarantors can be legal entities or individuals. Guarantees forwards, minors, and persons under the moratorium are strictly forbidden.

The guarantee shares the fate of the debt and follows it as an accessory right

The surety is a construction between three persons: the surety, the creditor, and the principal debtor with the creditor occupying a central place in this exchange (see Figure 1). According to article 492 paragraph 2 of the Swiss Code of Obligations, the accessory nature of a surety bond is defined as follows: “A surety bond can only exist on a valid obligation. A future or conditional obligation may be guaranteed if it becomes effective.

Figure 1 : Scheme on the construction of the guarantee – Swiss Banking Law Manual

The accessory nature of the guarantee is expressed by the fact that the guarantor can raise all the exceptions and objections that result from the debt relationship. The cancellation of this debt must be notified to the debtor as well as to the surety.

The rights of the surety

The surety may not renounce in advance the rights granted to him, but a later renunciation may be allowed. For example, if a surety bond is granted to secure an existing debt, it will be an acknowledgment of debt and the current prescription will be interrupted

Several requirements must be respected

To be valid, the guarantee must meet the following requirements:

The written form

The maximum amount

The name of the creditor

The signature of the surety

Indication of the guaranteed debt

The declaration of willingness to commit as a guarantor

Declarations of guaranty by individuals whose commitment exceeds CHF 2’000 require an authenticated form. The same applies to an increase in the amount of the commitment or the transformation of a simple guarantee into a joint and several guarantees. For other modifications such as the creation of a guarantee by a legal person or a commercial company, the written form will be sufficient.

For married persons, the modification of the guarantee can only be done if the spouse gives his consent. However, those who are not subject to this requirement are legally separated spouses, persons registered in the commercial register, owners of a private company, or as well as managers of a limited liability company.

Types of bonds

Simple Surety Bond

This is characterized by the fact that the guarantor can only be called upon after the creditor has found the debtor. The creditor can only demand payment if the debtor is bankrupt, has obtained a debt-restructuring moratorium, has a definitive certificate of default, and has transferred his residence abroad.

Joint and several guarantees

The joint and several guarantors can be sued before the search for the debtor and the realization of his real estate pledges, but on the condition that the debtor is in default with the payment of his debt. In other words, as soon as the debtor is in default, at the time of the first unpaid amount, the joint and several guarantors undertake to guarantee the defaults of the debt.

Joint guarantee

In the case of a simple joint guarantee, each guarantor is obliged for his share and as a guarantor for the share of the others. On the other hand, in the case of a joint and several guarantees, the guarantors commit themselves to the totality of the creditor’s debt.

Surety certifier and back surety

In this case, the debt by the guarantor is guaranteed. The creditor will be covered in the event of the guarantor’s insolvency. The guarantor has a right of recourse against the guarantor but also against the debtor.

As for the backup surety, it offers a guarantee to the surety and not to the creditor. Once the guarantor has taken action, he has a right to recovery after the payment against the principal debtor.

The “cautionnement romand” as an alternative in French-speaking Switzerland?

The “cautionnement romand” is an institution that carries out the missions conferred on it by the federal law of October 6, 2006, on financial assistance to guarantee organizations for small and medium-sized enterprises.

It can therefore guarantee operating or investment loans for individuals or companies to enable them to maintain an activity and develop jobs in the cantons of Fribourg, Vaud, Valais, Neuchâtel, and Geneva.

What are the conditions to be met to benefit from the “cautionnement romand”?

The maximum amount of the guaranteed credit is CHF 1’000’000.

Amortization period: 1 to 10 years.

Registration fee: CHF 300, which will be deducted in case of acceptance

One-time contribution to the expertise costs: 1% of the guaranteed credit (minimum CHF 500 and maximum CHF 2’700)

Risk premium: 1.25%.

Fixed fee for management and follow-up of the file: CHF 250

The applicant must first contact his bank to obtain a guaranteed loan. Applications must be made to the cantonal branch of the company’s headquarters. You must fill out a bond application form and attach all the documents and information required for the expertise as well as the registration fee. Once these elements have been received, expertise will be opened.

What is the reason for choosing a surety bond?

If we take the example of a rental, the surety bond is intended for all types of renters, whether they are individuals or professionals. All are concerned about the rental guarantee. Companies rent their offices, whether they are warehouses or offices.

The first solution is a bank deposit. The problem lies in the fact that the amount of the rent guarantee will often amount to 6 months for a commercial lease. This solution will generate a huge loss of income.

The deposit allows companies to put the money back into the production machine. This money represents a real source of investment. The money saved can be transformed into a cash flow that can pay off debts or maintain a cash reserve. For example, this money can be used to invest in communication, payment of suppliers, or purchase of goods.

By choosing this new form of guarantee, you opt for financial freedom and cash flow optimization.

The PrestaFlex team will guide you to the right solutions according to your needs. That’s why we have the resources to guarantee you a professional and quality service.

If you wish to obtain a loan to develop, innovate or invest in your company, we invite you to contact our teams on the website via the contact section. We handle your projects in the German and French-speaking parts of Switzerland and we offer you tailor-made financing and leasing solutions adapted to your situation.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.

These cookies are essential for the functioning of the website. They enable navigation, security and access to protected areas of the site. Without these cookies, the site cannot function properly.

These cookies allow the site to remember your preferences, such as language or region, and provide a personalized experience. They do not contain information that can personally identify you.

These cookies are used to display ads that are tailored to your interests. They do not store personal data, but use information about your behavior on the site to provide you with relevant ads.

These cookies collect anonymous information about how visitors use our site. This helps us analyze the data and improve the services and content we offer.

An excellent deal was concluded by our financing consultant Gabriel Oberson

An excellent deal was concluded by our financing consultant Gabriel Oberson  The success of swiss exports

The success of swiss exports